What is the Customs Clearance of Postal Items?

What is the customs clearance of international postal items?

- According to the Customs Act and the relevant international convention (Universal Postal Union), all international postal items are subject to customs inspection. This requirement is implemented for the purposes of customs and border protection such as securing tax revenues through the imposition of customs duties and blocking particular items for the protection of people’s health and national security.

- To achieve such goals, not all postal items are permitted to be carried into Korea but customs clearance of some postal items may be prohibited or restricted. In order to carry out tasks efficiently, customs offices intensively clear international postal items by designating customs clearance postal offices. Based on the customs inspection results, the goods are classified into duty-free goods, goods subject to import declaration and goods whose customs clearance is restricted.

- Duty-free goods cleared through customs are automatically delivered to the residence of the recipient and the postal items subject to customs clearance must go through the customs procedures before they can be received.

- In addition, each relevant customs office is randomly selecting exported postal items for inspection, and exporting any restricted goods, such as counterfeit goods, may result in punishment under the relevant laws.

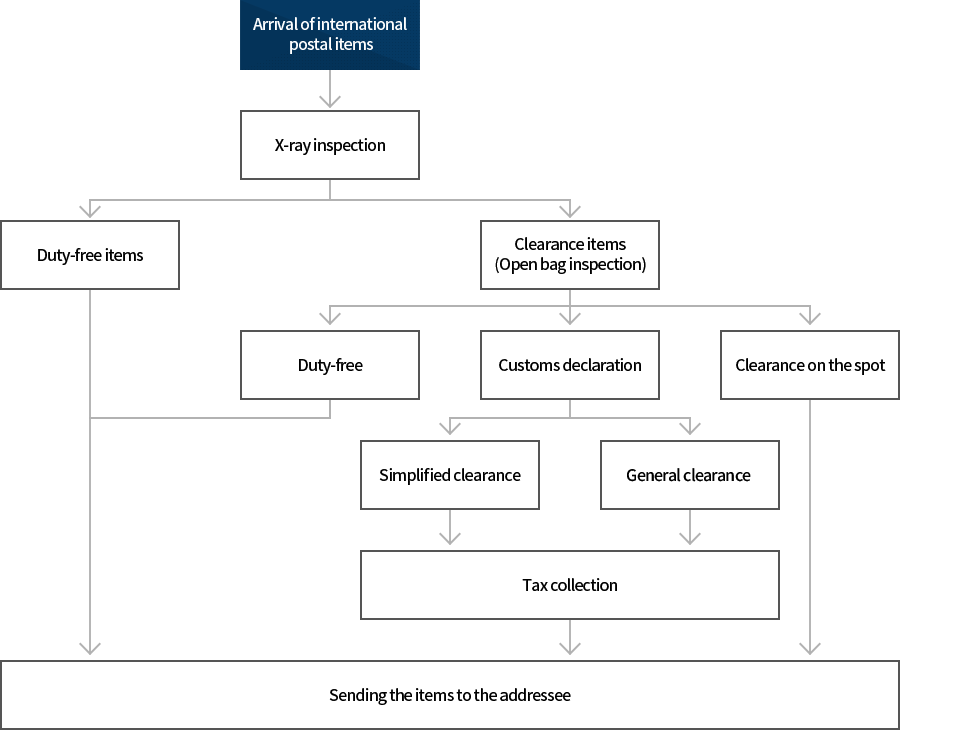

Flow chart for processing international postal items

Import clearance

- The postal items shipped or carried in from overseas are classified into goods subject to customs clearance and duty-free goods by the first customs inspection by X-ray. Each duty-free item is automatically sent to the recipient, and the goods subject to customs clearance need to go through the clearance procedures at the customs office.

- The postal items subject to customs clearance are again classified into goods subject to onsite taxation and goods subject to customs declaration (simplified or general clearance).

- The goods subject to onsite taxation are within the clearance allowance for postal items and have objective data required for determining the dutiable value (invoices, receipts, etc.). A duty is imposed on each of them, which is then delivered to the recipient. The clearance procedure for the postal item is completed when the recipient pays the imposed duty to the postman while receiving it.

- The goods subject to customs declaration require necessary data for determining the dutiable value or may have import restrictions. The relevant customs office sends a postal item clearance guide to the owners (recipients) of such goods to provide information on the simplified or general import declaration procedures. The procedures are as follows:

- Simplified and general declaration procedures

- Goods subject to customs duties

- Goods tended for personal use, such as for use as gifts, the sum of whose value and the postal charges, etc. exceeds US$150

- Company goods, commercial goods, etc. (However, goods recognized as samples with a value of not more than US$250 are exempt from duties.)

- Methods of declaration, required documents, etc

Methods of declaration, required documents, etc Classification Simplified Declaration General Declaration Goods subject to declaration - Postal items subject to customs clearance other than those subject to general import declaration

- Items which need to be confirmed by the head of the customs office under Article 266 of the Customs Act (including items whose export and/or import are restricted or prohibited)

- Goods which are shipped or carried in for the purpose of being sold

- Purchased goods which exceed the value of US$1,000

Application - Submit data after selecting one from among Mobile, Internet, Email, Fax, Mail, and Visit

- Air mail items must be declared to the head of the Incheon Airport International Postal Customs and sea mail items to the head of the Busan International Postal Customs through customs brokers, etc.

Required documents - Application form for the simplified clearance of international postal items

- Price data such as the receipt, the invoice, etc.

- In the case of re-imported items: Original copy of the export declaration completion certificate (or documentary evidence of export)

- Import declaration form

- Price data such as the invoice

- Value declaration form

- Required documents for import (in the case of the relevant items)

Internet - (Mobile) http://m.customs.go.kr

- (PC) http://unipass.customs.go.kr

FAX - (Air mail items) 82-32-720-7491, 7492

- (Sea mail items) 82-55-367-7016

E-mail - (Air mail items) minwon9@customs.go.kr

- (Sea mail items) onestop7013@customs.go.kr

- Goods subject to customs duties

Export clearance

Goods subject to simplified export declaration

All exported goods can be exported to foreign countries after the completion of the required export clearance procedures under the Customs Act, but the items mentioned below can be exported by mail without having to go through the process of filing any extra export declaration with the customs office.

- Mass media news materials such as newspapers, new coverage films, recording tapes, etc.

- Catalogues, records and documents

- Goods purchased by foreign tourists in accordance with the Special Regulations on the Value Added Tax and the Special Consumption Tax for Foreign Tourists, etc.

- Non-refundable items whose price is not more than FOB 2,000,000 won (However, the items subject to confirmation by the head of a customs office under Article 226 of the Customs Act are excepted.)

Prohibited items for export

The postal items prohibited from being exported to foreign countries are as follows, and violation of this prohibition may result in punishment under the relevant regulations.

- Books, publications, pictures, movies, music records, video works, sculptures or any other items of similar nature that may disturb the constitutional order or be harmful to the public security or social customs

- Items which may be used to disclose any confidential information of the government or engage in spy activities

- Counterfeit or altered items or replicas of money, bonds or other marketable securities

- Items which may infringe upon intellectual property rights such as counterfeit goods