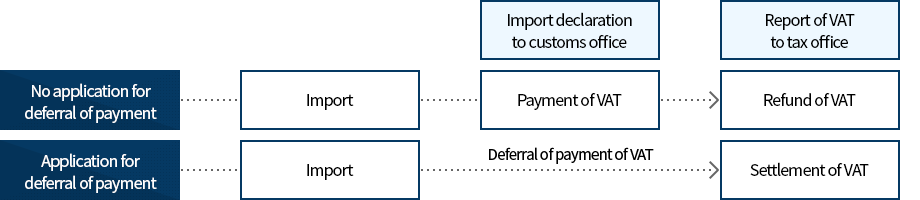

Deferred Payment of VAT on Imported Goods

Applying for Deferred Payment of VAT on Imports

Details of the scheme

Through the deferred payment scheme, small or medium business owner or middle-standing business owner may apply the deferred payment of value-added tax on the importation until the report of the settlement of VAT to the tax office. (Article 50-2 of the Value-added Tax Act)

Overview of Deferred Payment of VAT on Imports

The following are the subjects of deferral of payment of VAT (Article 91-2 of the Enforcement Decree of the Value-added Tax Act):

- 1 Small or Medium business or middle-standing business (Articles 2 and 10 of the Enforcement Decree of the Restriction of the Special Taxation Act)

- 2 Small & Medium Enterprise〕 The ratio of exports to the total value of goods or services is at least 30 percent, or the amount of such exports is at least ten billion won 〔 Middle-Standing Company〕 The ratio of exports to the total value of goods or services is at least 50 percent

- 3 Business has been operated for the past 3 years

- 4 No record of failing to pay the customs duty or national tax for the past 2 years

- 5 No record of being punished for violation of the Customs Act or Punishment of Tax Offenses Act for the past 3 years

- 6 No cancellation of the approved deferral of payment for the past 2 years

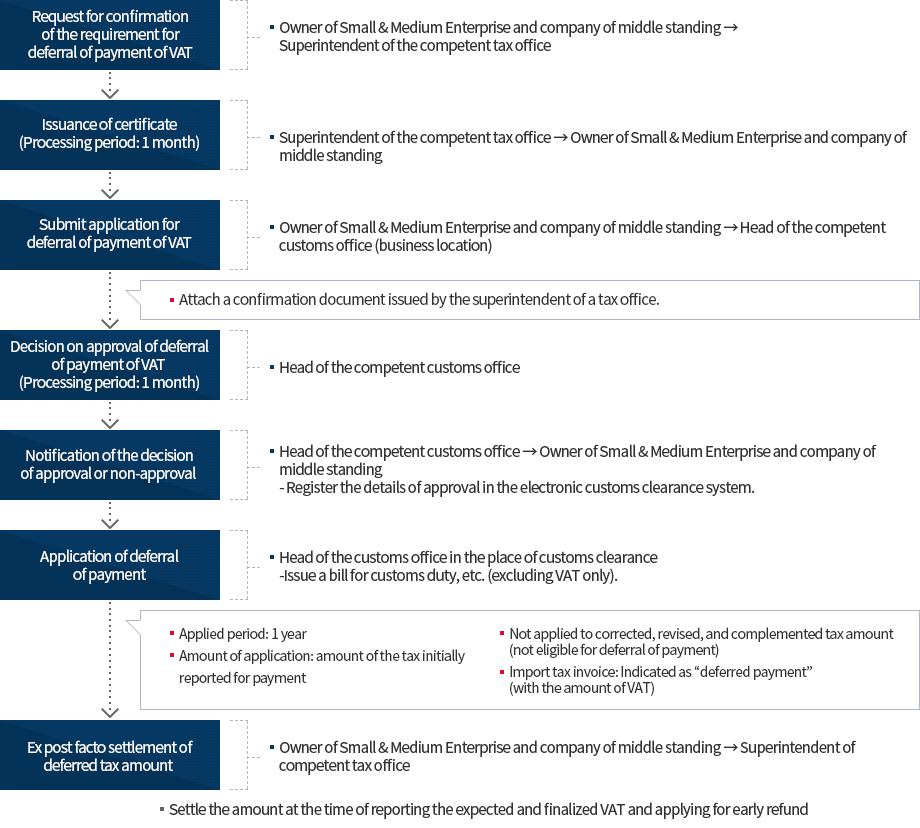

The application procedure of Deferred Payment of Import VAT

For more information

Korea Customs Service, Audit Policy Division, 042-481-7754